After the stock market’s fantastic growth in 2021, many believe a pullback (or even a correction) may be a healthy thing. Such a drop is not horribly painful, by historical standards, and smart investors can cushion such a fall.

Why is a market correction beneficial? Because it prevents another bubble from forming. Bubbles occur when stock prices get clearly out of line with the earnings potential of the underlying companies. We saw the consequence of that in the awful 2000-02 and 2008-09 market wipeouts when some people lost half their wealth or more.

Certainly, market corrections never feel healthy when they occur. People get fearful as the market declines, the media fan the flames by giving investors reason after reason to be afraid, and worries that this is the beginning of the next crash.

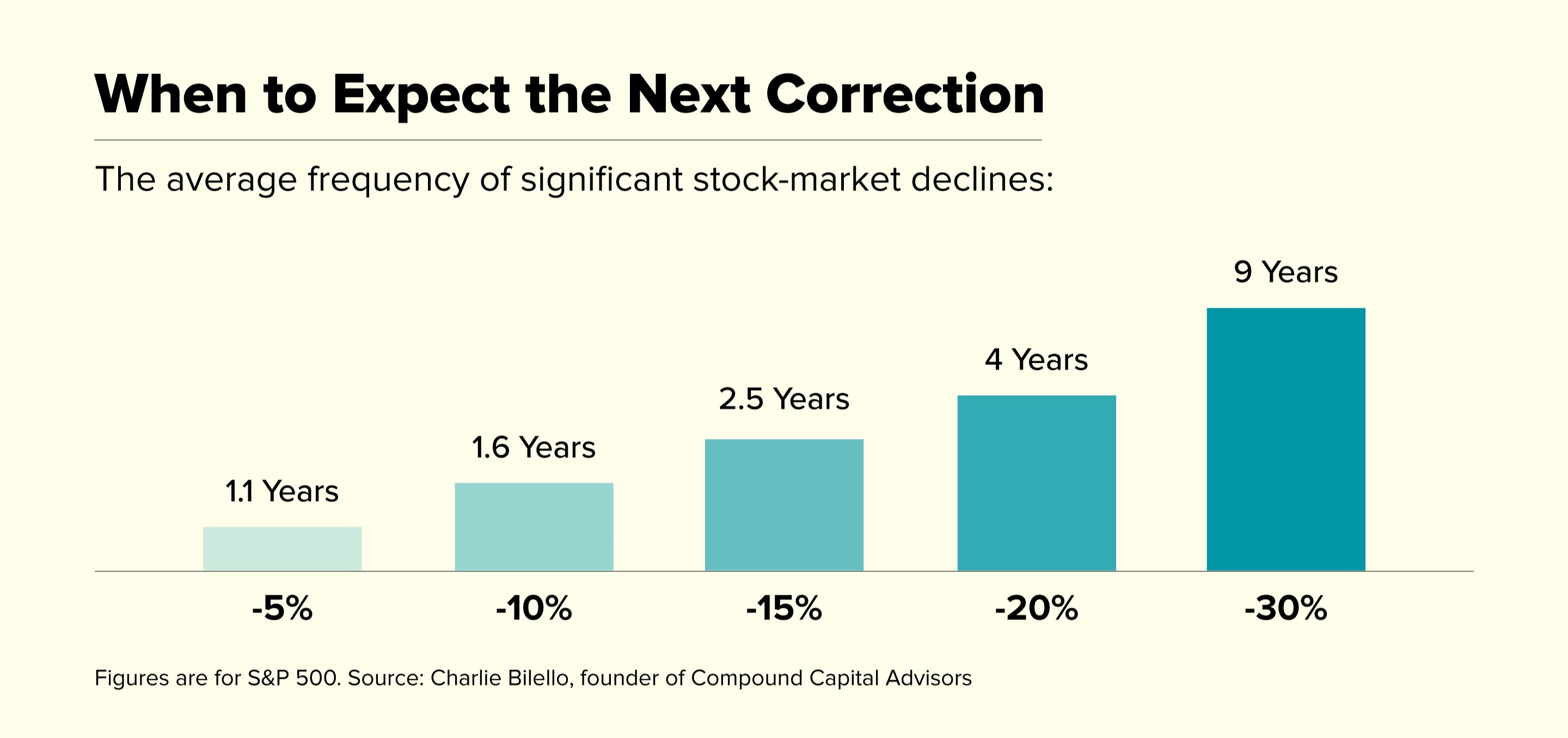

But did you know that since 1950, the S&P 500 has experienced an intra-year peak-to-trough pullback of 5% or worse in 67 out of 70 years? So roughly 93% of the time, a 5% correction has taken place from 1950-to 2021.

While many investors admit that a 5% pullback is manageably unpleasant, concerns expand when the market decline hits 10%.

When is the Next Correction Coming?

Here is what investors need to remember: the S&P 500 has nearly doubled in value since the market turmoil in March 2020. What has not happened since that time, however, is a selloff of at least 10% - that’s the definition of a market correction.

Further, in 29 of the past 50 years, the S&P 500 has experienced a 10% correction. And since 1928, market corrections happen about once every 19 months. But guess when the last market correction occurred?

That would be 19 months ago.

How to Prepare for a Correction

Are you thinking: “I don’t think I can stomach a loss of 10%?” Then that’s where the wisdom of diversification can become apparent.

Remember that the data above represent the historical performance of the S&P 500, an index composed of 100% stocks.

A financial professional can help you manage an asset allocation mix of stocks, bonds and cash that represents your tolerance for risk. Consequently, your portfolio likely isn’t 100% stocks. In fact, the appropriate allocation for an average investor approaching or already enjoying retirement might be closer to only 50% stocks. This means that on average, your portfolio should decline only half as much as the S&P 500 during market downturns.

So proper diversification can bring you back to the “manageably unpleasant” range. But if not, you may need to reevaluate your risk tolerance to avoid exposing your nest egg to a larger loss than you can endure.

Although the recent market pullback may produce lots of fear, we’ve been here before.

_____________________________________________